Your traditional IRA is not a ticking tax bomb

The math might surprise you

A woman I spoke with recently told me she’s worried about her traditional IRA.

Not because of the market.

Because she’d read that her retirement savings were “infested with taxes” and she’d made a terrible mistake by not converting everything to a Roth IRA years ago.

She’s not alone.

If you have a significant balance in a traditional IRA or 401(k), you’ve probably heard some version of this message.

The financial media loves the phrase “tax bomb.”

Other advisors love to tell you that Roth conversions are the only sensible strategy.

Your friends may have told you what they did and made you wonder if you missed the boat.

Here’s the idea: the taxes on your traditional IRA in retirement are almost certainly not as bad as you’ve been told.

And the fear is probably worse than the reality.

Let me show you what I mean.

A quick example with round numbers

Meet Carol and David.

They’re both 75 and happily retired. Here’s what their financial picture looks like:

$2.5 million in a traditional IRA

$150,000 in savings

$80,000 per year in combined Social Security

A paid-off home

That $2.5 million IRA is something to be proud of.

They saved consistently over decades. They made good decisions. And now the IRS says they have to start taking money out each year through required minimum distributions.

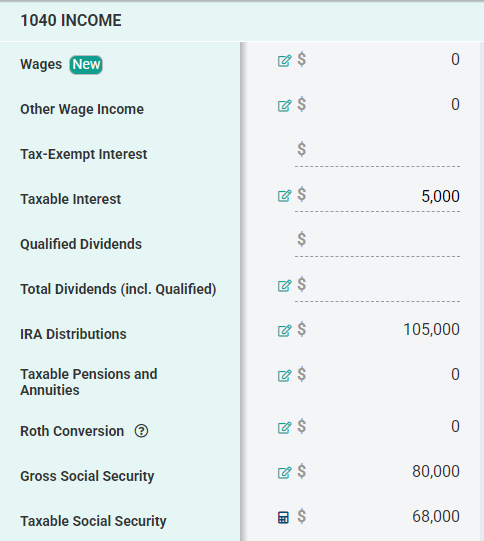

In 2026, their IRA RMD is roughly $105,000.

Combined with Social Security and a little interest income, their total gross income for the year is around $178,000.

Now here’s where the fear usually kicks in.

Most people hear “$178,000 in income” and assume the worst.

But let’s look at what actually happens on their tax return.

How the tax math actually works

First, not all of their Social Security is taxable.

About $68,000 of their $80,000 in Social Security shows up on their tax return. This is the 85% maximum of Social Security income that can be taxed.

Which means $12,000 of their Social Security benefits are tax-free.

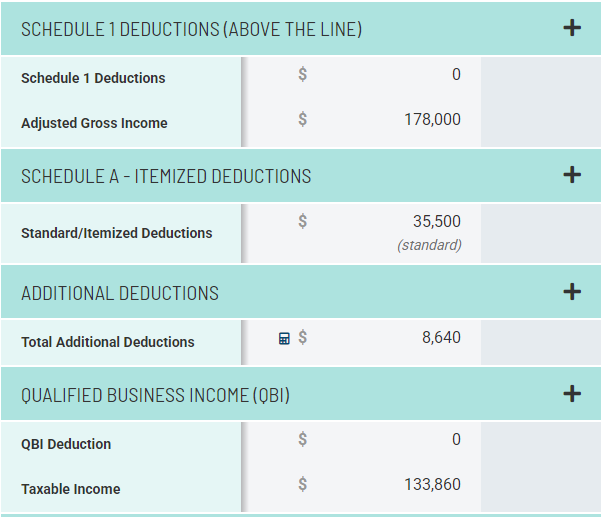

After their standard deduction and the additional deduction they get as seniors, their taxable income drops to roughly $134,000.

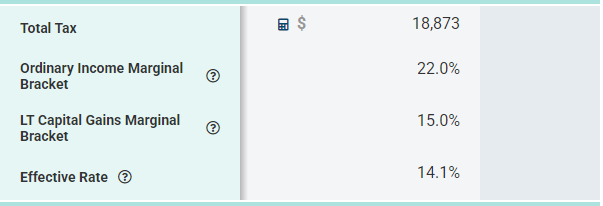

Their federal income tax?

Approximately $19,000.

That’s an effective tax rate of about 14% on their taxable income.

Let me say that again.

A married couple with a $2.5 million traditional IRA, taking a six-figure required minimum distribution, pays about 14% in federal income tax (relative to their total taxable income).

Put another way, out of their $178,000 gross income Carol and David, only about 11 cents goes to the IRS.

Is that zero?

Absolutely not.

But is it the tax bomb you’ve been warned about?

Not even close.

Where does the RMD actually land?

Here’s the part that surprises most people.

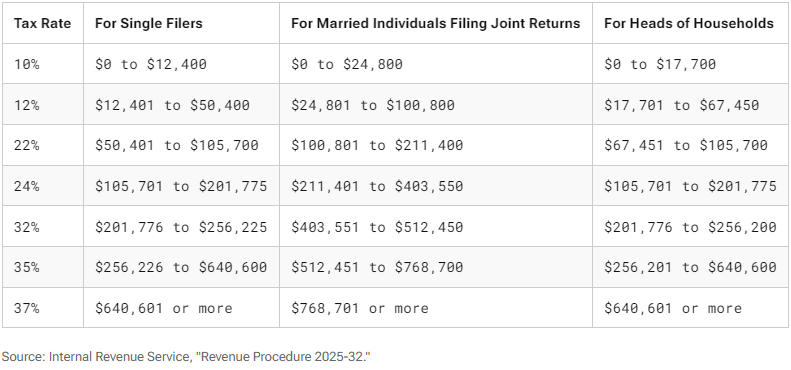

That $105,000 required minimum distribution doesn’t all get taxed at the same rate. It gets stacked on top of their other income and flows through the brackets like water filling buckets.

Some of it lands in the 10% bracket. A good portion lands in the 12% bracket. And only a slice reaches the 22% bracket. None of it touches 24% or higher.

Here’s a quick refresher on how our income tax brackets work:

If Carol and David deducted their 401(k) contributions years ago at 22%, 24%, or even higher rates while they were working, they’re coming out ahead.

They saved at a higher rate.

They’re now paying at a lower rate.

That’s exactly how this was supposed to work.

What about IRMAA?

If you’re on Medicare, you may have heard of IRMAA — the income-related surcharge that increases your Medicare premiums. It’s a real concern at higher income levels.

But Carol and David?

Their modified adjusted gross income falls below the threshold. No IRMAA surcharge. Even with a $2.5 million IRA.

This doesn’t mean IRMAA will never apply to you.

If your income is higher, or if you have a large capital gain in a given year, it could.

But it’s another example of something that sounds scary until you look at your actual numbers.

With your most recent tax return and some simple projections, we can reference data like this to make smarter decisions:

A note about qualified charitable distributions

If Carol and David are charitably inclined — and many of my clients are — they could use a qualified charitable distribution to send some or all of their RMD directly to charity.

And avoid taxation on these dollars.

A QCD satisfies the RMD requirement, supports the causes they care about, and reduces their adjusted gross income.

It’s one of the most tax-efficient ways to give, and it’s available to anyone over 70 1/2 with a traditional IRA.

The important caveat

I’m not here to tell you that Roth conversions are a bad idea.

They can be a powerful strategy when the timing and circumstances are right.

And at higher IRA balances the tax math does change.

The RMDs get larger, the tax brackets get higher, and strategies like Roth conversions earlier in retirement can make a real difference.

But the mistake I see most often isn’t failing to convert.

It’s assuming a one-size-fits-all solution based on a headline, a rule of thumb, or what a friend did.

Just because Roth conversions made sense for someone you know doesn’t mean they’re the right move for you.

As with most things in personal finance, the honest answer is: it depends.

What to do next

Put your lifestyle first. Never let the tax tail wag the dog. Your retirement savings exist to support the life you want to live, not to win a tax optimization contest.

Take a holistic view. Make sure you or your advisor reviews your tax return each year and builds proactive tax planning into your decisions. Taxes are one piece of a larger puzzle that includes income, spending, investments, and estate planning.

Don’t over-optimize for taxes. Over-optimize for living your best possible life with the money you have. A slightly higher tax bill in service of a life well-lived is not a failure. It’s the whole point.

Bottom line

Your traditional IRA isn’t a ticking tax bomb.

It’s a retirement paycheck you built over a career of smart saving. And with the right guardrails in place you can spend your energy on living instead of worrying.

If any of this raised a question, please reply or reach out if you’d like to discuss it further.

Links & things

I was happy to have received - for the 2nd year in a row - the 2026 Wealthtender Voice of the Client Highly Rated Advisor award.

Thanks to my clients for their trust and generous reviews which you can see here.

Thank you for reading!

If you’re not a client and would like my advice, simply reply to this email with your questions and I’ll be happy to respond with my thoughts…

Until next Wednesday,

Russ

Right on Russ! I have seen so few people detailing that conversions aren’t always what they’re cracked up to be. Do you own due diligence and make a decision based on your personal preferences, consider that it won’t be a panacea that it’s often made out to be.