Your greatest retirement risk

Why inflation matters more than you think — especially for women

When you think about retirement, what comes to mind?

Travel?

More time with family?

A new hobby?

Something else?

Or a long list of something elses?

All of those are great.

But here’s something I think about a lot — and most people don’t:

How much will a gallon of 2% milk cost in 25 years?

It may sound a little silly.

But this isn’t about milk.

It’s about how your money stretches — or doesn’t — as life moves on.

The Quiet Force That Changes Everything

Inflation is the rise in prices over time.

But here’s the thing most people miss:

Inflation doesn’t hit everything equally.

Some costs rise slowly.

Others jump faster.

And over 20 or 30 years in retirement, those jumps can really add up.

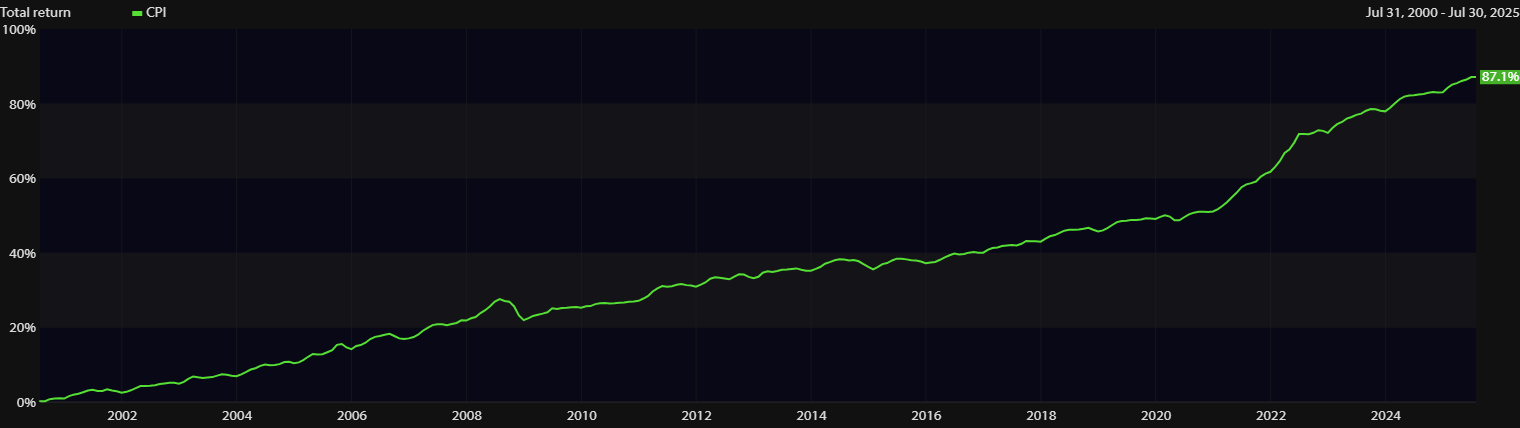

Here’s what inflation - as measured by the Consumer Price Index (CPI) - looked like for the last 25 years:

The chart above shows an 87% increase in prices (as measured by CPI) over 25 years.

Some folks argue inflation is much higher than currently reported.

While others suggest that how inflation is calculated needs to be updated.

What no one disputes?

That prices go up over time…

A Few Quick Numbers (and why they matter)

Let’s say inflation averages about 3% per year.

That’s a long-term average. Perplexity confirms this.

But some expenses often rise faster than that.

Others may rise more slowly or even get cheaper.

Here’s what a few everyday items might cost in 25 years (assuming 3% annual inflation):

Gallon of milk:

$4.50 → $9.40

Dozen eggs:

$3.75 → $7.80Gallon of gas:

$3.85 → $8.00Dog food:

$65 → $135First-class postage stamp:

$0.78 → $1.63Movie ticket:

$12 → $24.50New car:

$45,000 → $93,000New home (average):

$450,000 → $930,000+

These are estimates, not predictions.

Some - like TVs - may end up lower.

Others — especially housing or healthcare — could be much higher.

That’s not to scare you.

But it’s important to understand the impact on your spending.

And your lifestyle.

Not Everything Calls for a Spreadsheet

I’m not saying you need to track every penny or overthink your grocery list.

But I am saying this:

If you want to maintain your lifestyle over a retirement that could easily last 25 years (or more), your money needs to grow — because prices certainly will.

Some clients tell me, “I don’t spend that much now, and I don’t expect to spend a lot later.”

But retirement isn’t immune to the ravages of inflation.

Your spending may shift over time (more travel early on, more medical care later).

Some costs may shrink, others will grow.

The real risk is assuming today’s dollars will carry you through the rest of your years.

Why This Hits Women Especially Hard

Women live longer.

They’re more likely to handle household expenses on their own at some point.

And many expenses that rise faster — like food, healthcare, and housing — may affect women most over a 25+ year retirement.

That’s why inflation matters.

It’s not just numbers and statistics.

It’s a very real factor in your life story.

What You Can Do Now

You can’t control inflation.

But you can plan for it.

Here’s how I help my clients:

Build an income plan that is resilient and adjusts over time

Keep your money invested and growing throughout retirement

Add flexibility for life’s curveballs

Focus on what you value, not just what your friends & family are doing

Use smart tax strategies to help your money go further

A Gentle Nudge

Thinking about prices going up is no fun.

But planning for it?

That can lead to clarity, confidence, and comfort.

And calm…

Because when your money is calm, your life can be more exciting!

You’ve worked long and hard to build a good life.

Let’s make sure you can keep living it — whether milk costs $5 or $15.

If you’d like help thinking this through — or just want to talk about what your numbers look like — I’m here.

What will a movie ticket will cost when you’re 85?

Better question: will you be able to afford popcorn too?

I appreciate your continued readership.

Please let me know if you have any feedback or suggestions for future essays.

Until next Wednesday,

Russ