Why averages are terrible guides for retirement decisions

Why comparing yourself to benchmarks creates anxiety instead of confidence

Nassim Nicholas Taleb has a quote I love:

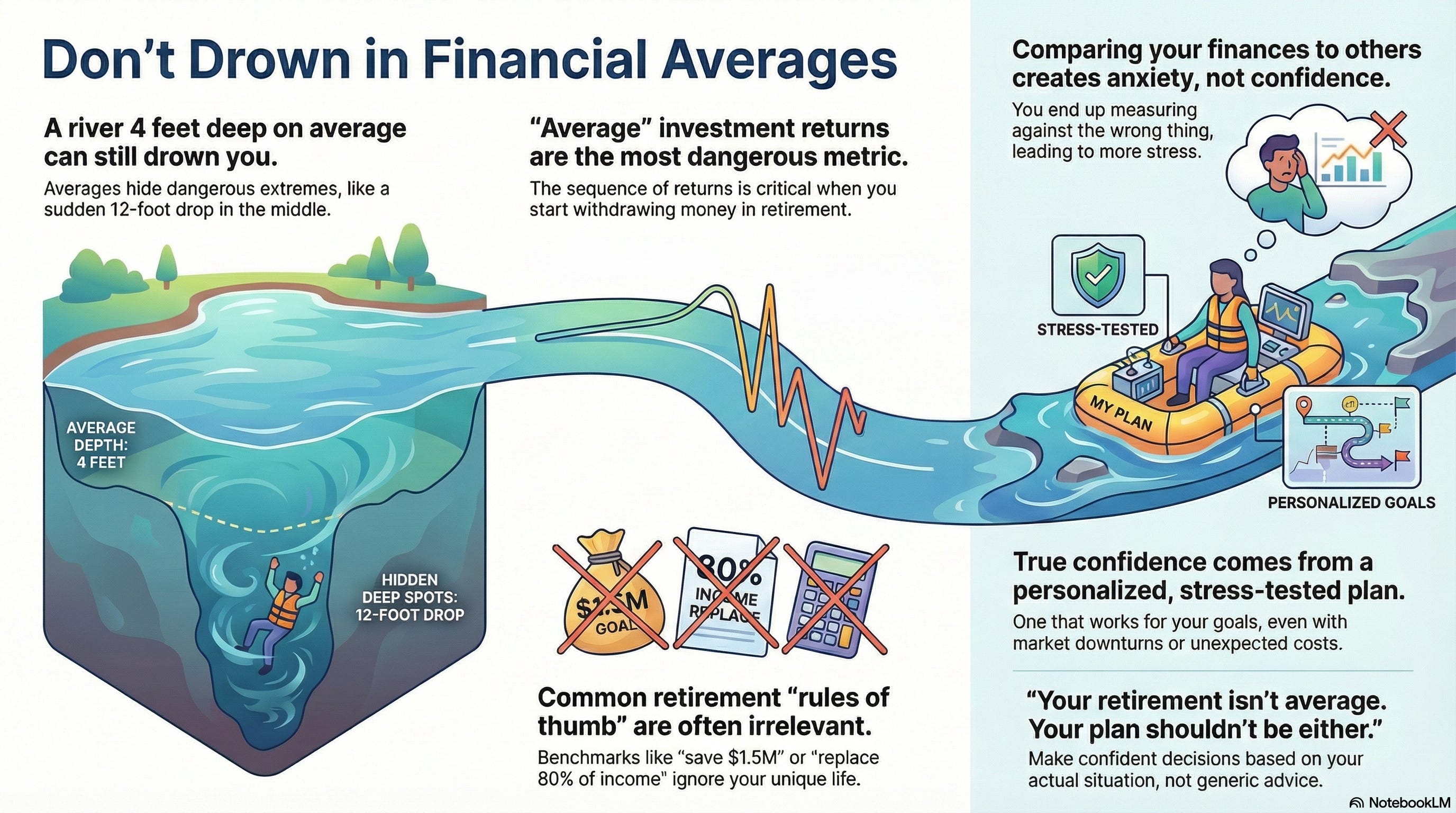

“Never cross a river that is on average four feet deep.”

It’s a vivid image.

You’re standing at the edge of a river.

Someone tells you the average depth is four feet.

Sounds manageable, right?

You could probably wade across.

Except that average might mean it’s two feet deep for most of the way—and twelve feet deep in the middle.

If you can’t swim… well, that’s a problem.

You may drown.

The average told you nothing useful about your actual experience crossing that river.

I see this same problem constantly in retirement planning.

Except instead of rivers, we’re talking about investment returns, savings benchmarks, and retirement income needs.

But instead of drowning, you lie awake at 3 AM wondering if you’re going to run out of money.

“How do I compare to your other clients?”

I get asked some version of this question regularly.

“Am I ahead of where I should be?”

“Do your other clients have more saved than I do?”

“Is my spending higher than average for someone my age?”

I understand why people ask.

It feels like comparing yourself to others, or to some average, should provide clarity.

Maybe even confidence.

If you’re above average, you must be okay, right?

But here’s what I’ve learned after more than 30 years: Comparing yourself to averages or to other people’s situations doesn’t create confidence.

It actually creates more anxiety.

Because you’re measuring against the wrong thing.

The most dangerous average: investment returns

Let me show you what I mean with actual numbers.

A few months ago, I shared several portfolios that all averaged 8% returns. Click below to read the essay.

The article above shows several examples of the same average return over the same time period.

But depending on the actual sequence of those returns, especially in those critical early retirement years, the outcomes were dramatically different.

Here’s why this matters so much for women in their late 50s and 60s:

When you’re working and contributing to your portfolio, return sequence doesn’t matter much.

Bad years?

They get smoothed out by good years. Time is on your side.

But when you retire and start taking distributions to fund your life?

Your actual experience (sequence of returns and not average returns) becomes super important.

If you retire into a bear market and start pulling money out while your portfolio is down, you lock in losses.

You sell shares at depressed prices.

And when the market eventually recovers, you own fewer shares to participate in that recovery.

Two people with identical portfolios, identical average returns over 20 years, and identical spending can end up in completely different places.

One might have $3 million left.

The other might be broke.

Same river. Same average depth.

One person gets across safely.

The other drowns.

The average return tells you nothing about whether you’ll be okay.

Other dangerous averages

This problem shows up everywhere in retirement planning.

“The average retiree needs $1.5 million.” Maybe. But what if your house is paid off and you have a pension? What if you want to travel extensively for the first decade of retirement? What if you’re planning to help your grandchildren with college? Your number might be $800,000. Or $4 million. The average is irrelevant. (I've written about the problems with averages before.)

“You’ll need 80% of your pre-retirement income.” This rule of thumb assumes your expenses stay roughly the same forever. It ignores that you’re no longer saving 15% of your income. It ignores that your mortgage might be paid off. It ignores that spending typically follows a pattern: higher in your 60s (the “go-go years”), lower in your 70s (the “slow-go years”), and higher again in your 80s for healthcare (the “no-go years”). Eighty percent might be wildly wrong for you.

“Stocks return 10% on average.” Sure, over very long periods. But what about the money you’ll need next year? Or in three years? Your experience might be 15% returns. Or negative returns. The average doesn’t help you sleep at night when you’re trying to decide if you can retire in August.

Where real confidence comes from

Here’s what I tell clients who ask how they compare:

It doesn’t matter.

What matters is whether your plan works for your life.

Can you travel in your 60s without guilt?

Can you help your daughter buy a house and still be fine?

If the market drops 30% next year, will you still sleep soundly at night?

Can you give generously to the causes you care about without wondering if you’re being reckless?

That’s where confidence comes from.

Not from knowing you’re “above average.”

Not from comparing yourself to your sister or your neighbor or some benchmark in a magazine article.

Real confidence comes from having a personalized plan built on your actual situation—your resources, your spending, your timeline, your definition of enough.

It comes from knowing that we’ve stress-tested your plan against bad sequences of returns, against living to 97, against higher-than-expected healthcare costs. And it still works.

It comes from knowing the specific actions you need to take—not generic advice for “people like you,” but decisions tailored to your life.

Don’t cross that river

Averages can be useful for understanding general patterns or trends.

But they’re terrible guides for individual decisions.

You can’t build a reliable plan on average returns.

You can’t fund your life with average savings.

You can’t make confident decisions based on what other people are doing.

The river might be four feet deep on average.

But if you’re five feet tall and there’s a six-foot drop in the middle, that average could drown you.

Your retirement isn’t average.

Your life isn’t average.

Your plan shouldn’t be either.

Thank you for reading!

If you ever have any feedback or suggestions for me, simply hit reply or leave a comment and share what’s on your mind…

Until next Wednesday,

Russ

Confidence really does come from understanding your own situation, not measuring against others.