Beyond the portfolio: Why women need more than investment management

Investments are important, but they're just a part of your retirement planning

You’ve worked hard for decades.

You’ve built a successful career.

You’ve saved money.

Your investment accounts show it—maybe $2 million, $5 million, or more.

So why do you still worry?

Why do you wake up at 3 AM wondering if you’ve thought of everything?

You’re not alone in your worry

Here’s something that might surprise you.

You’re not the only one who feels this way.

A recent study by Fidelity found that 81% of women say money worries keep them up at night.

Not just impoverished women. Women at all income levels.

Even successful women like you.

What worries them most?

Paying for emergencies.

Dealing with rising prices.

Having enough money to enjoy life.

Saving for the future.

Notice what’s NOT on that list?

Whether their investments went up or down this month.

The worry isn’t about your portfolio.

It’s about what your portfolio can help you do and achieve.

It’s about whether you’ve covered everything.

Whether you’re truly ready.

Whether your plan will work when life gets hard. Or surprises you.

The problem with most financial advisors

Most financial advisors at big firms work with 150 to 200 (or more) clients.

They meet with you once a year (maybe).

They show you some colorful charts and a portfolio performance report.

And they call it financial planning.

But that’s not real planning.

Managing your investments is just one piece of a much bigger puzzle.

For women especially, the other pieces matter just as much. If not more…

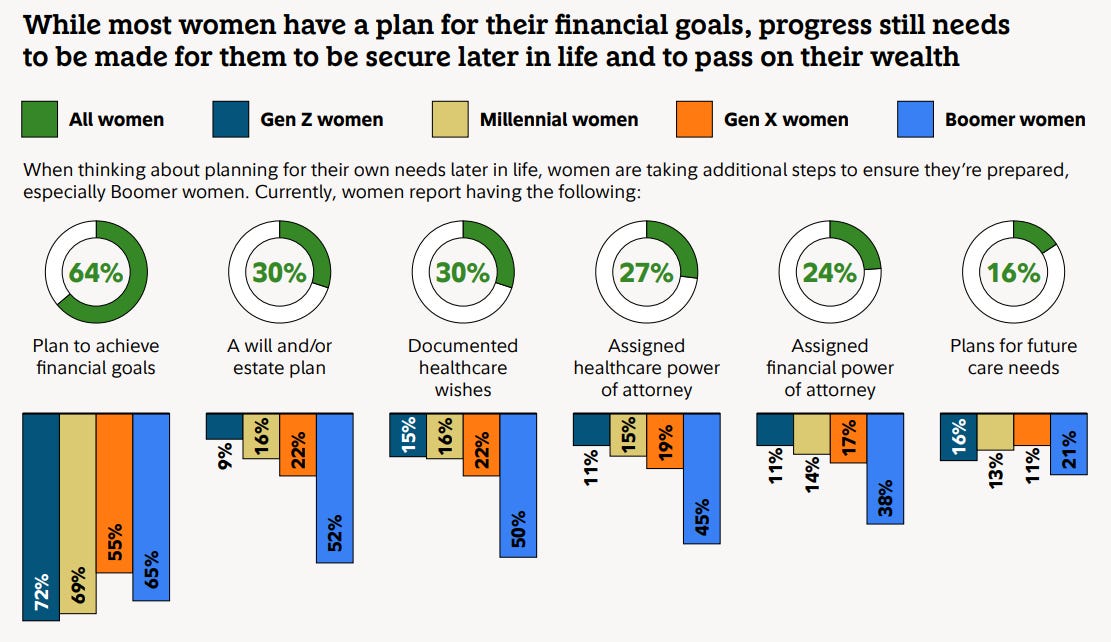

Look at these numbers from the same study:

Only 30% of women have a will or estate plan

Only 27% have assigned someone to make healthcare decisions if they can’t

Only 24% have assigned someone to handle their money if they can’t

These aren’t investment decisions.

But they ARE planning decisions. Important ones.

If your advisor doesn’t look at your tax return, doesn’t ask about your insurance, and never talks about what happens if you get sick... you’re not getting financial planning.

You’re just getting investment management.

No wonder you still worry.

What real planning looks like

Real financial planning gives you peace of mind.

It answers the big questions that keep you up at night:

Can you afford to retire? Not just “do you have enough money saved?” But can you live the way you want for 30+ years? What if you live to 95? What if you need help at home or in a facility? What if prices keep going up?

Are you paying too much in taxes? When did your advisor last look at your tax return? Many never ask to see it. But good tax planning can save you hundreds of thousands of dollars over your lifetime.

What happens if something happens to you? Do you have updated documents? Have you named someone to make decisions if you can’t? The Fidelity study found that 75% of women think they could handle the money if their partner died. But feeling confident isn’t the same as being prepared.

Is your insurance right for you now? When did you last review your policies? Are you paying for coverage you don’t need? Or missing coverage you do need?

How will you create income in retirement? Saving money is one thing. Turning it into monthly income that lasts your whole life is another. Which accounts should you use first? How do you pay less in taxes? When should you claim Social Security?

These questions are all connected.

They need to be looked at together, not separately.

Why this matters even more for women

The Fidelity study revealed something else.

Women face special money pressures that many advisors ignore.

Almost half of women (45%) say they can’t leave their jobs right now.

Many feel stuck.

They’re not happy at work, but they don’t feel like they can quit.

Women also have less in savings than men. On average:

Women have $47,000 in savings versus $62,000 for men

Women have $36,000 in emergency funds versus $54,000 for men

21% of women have no savings at all

If you feel trapped in a job that drains you, retirement planning isn’t just about money.

It’s about getting your life back. Now, not after you’ve retired…

The kind of help you deserve

Here’s what I’ve learned over 30+ years as a financial advisor.

The clients who sleep best at night aren’t the ones with the best investment returns.

They’re the ones who know they have a solid plan.

They have an advisor who helps them look at the whole picture.

They know:

Their retirement income will last

Their taxes are handled well

Their estate plan matches what they want

Their insurance makes sense

Someone is watching the details so they don’t have to

That’s not just investment management. That’s a real partnership.

And it needs a different kind of relationship.

Not just once-a-year meetings with someone who has 200 other clients competing with you for their time and attention.

Questions to ask any financial advisor

If you’re looking for a financial advisor, ask these questions:

Do you look at my tax return every year? If they say no, they’re not doing real planning. Tax planning is one of the most valuable things an advisor can do. But many skip it.

How many clients do you have? If it’s over 100, ask yourself: How much time can they really give me? Will they truly know my situation?

What happens when I have questions about insurance or estate planning? Do they help you? Or do they send you somewhere else?

Will you show me if I can really retire? Not just “you have enough money.” A real plan that shows where your income comes from and how long it will last.

Are you a fiduciary? And do you serve as a fiduciary for your clients at all times? Some advisors (like me) do; many more do not.

Their answers will tell you if they’re a true partner or just an investment manager.

The peace of mind you want

I can’t make every worry go away.

Markets will still go up and down. Unexpected things will still happen. Life is always unpredictable.

But here’s what I can do.

I can give you a clear, simple plan that shows you’ll have steady income for the rest of your life.

A personalized plan that covers your investments, your taxes, your insurance, your estate, and all the other details that matter. To help you live a life that matters to you.

That’s what turns worry into peace of mind.

That’s what lets you stop wondering if you’ve thought of everything.

That’s what lets you retire with clarity and real confidence.

Not just money in the bank, but the ability to live life your way.

You’ve worked hard. You’ve saved a lot.

You deserve financial planning that helps you live the life you’ve been dreaming of.

After reading the above, please review the following “Master List of Goals”

Did you notice that while many of the goals in the list above relate directly to investment management, many of them do not…

There’s much more to real financial planning than investment management.

I appreciate your continued readership.

Please let me know if you have any feedback or suggestions for future essays.

Until next Wednesday,

Russ