A deep dive into the Coca-Cola Company 401k

As an employee of The Coca-Cola Company (TCCC) here in Atlanta, Georgia, you may be eligible to contribute to the company’s 401k. A 401k is a company-sponsored retirement savings plan. Typically, employees who are eligible to contribute make pre-tax contributions to their Coca-Cola Company 401k.

You continue to contribute up until you retire, and your contributions are invested in funds that you choose based on your savings goals and retirement timeline. Then, you take Required Minimum Distributions (RMDs) from the account after you enter retirement and pay taxes on the income you withdraw.

Every company’s 401k plan is a little bit different, but there are a few key things to know about The Coca-Cola Company’s plan:

Not all employees are eligible to contribute

TCCC has specific default elections for their 401k

There are contribution limits

TCCC offers a company match

Let’s examine what you can expect from your 401k plan and how to leverage your savings for an ideal retirement.

Who is Eligible to Join the Coca-Cola Company 401k?

To enroll in TCCC’s 401k plan, you must be a United States citizen or a permanent resident who has worked for Coca-Cola for 30 consecutive days or more. However, there are a few exceptions to this. You aren’t eligible to enroll if you are:

Already enrolled in a different defined compensation plan

A leased employee

Covered by a “collective bargaining agreement”

Essentially, TCCC only allows workers who are full or part-time W2 employees who have worked for 30 days straight to enroll. Contractors and employees who are “leased” by Coca-Cola from another entity aren’t eligible.

Who is the Coca-Cola 401k Provider?

The Coca-Cola Company 401k plan is administered through Transamerica Retirement Solutions, one of the country’s largest retirement plan administrators. Once you’re eligible, you’ll access your account through Transamerica’s online portal, where you can check your balance, update your contributions, and choose how your money is invested.

You’ll have various investment options to pick from—including mutual funds, target date funds, and other professionally managed portfolios. These choices give you the flexibility to tailor your investments based on how long you have until retirement and how much risk you’re comfortable taking.

How to Enroll and Default Elections

The good news is that enrolling in the Coca-Cola Company 401k is easy – because they do it for you! All eligible employees are automatically started on a plan and are given an enrollment deadline to select their contributions. Most people choose to actively enroll and select their options before their enrollment deadline. This puts you in the driver’s seat of your 401k and can help you to make elections that align with your retirement goals.

However, if you choose to let TCCC auto-enroll you in their 401k, here are the contributions they set up for you:

When auto-enrolled, TCCC will initially contribute 3% of your salary to your 401k. Then, annually, TCCC will increase your contributions by 1% until you reach a 6% total annual contribution. Remember, you can change your enrollment at any time.

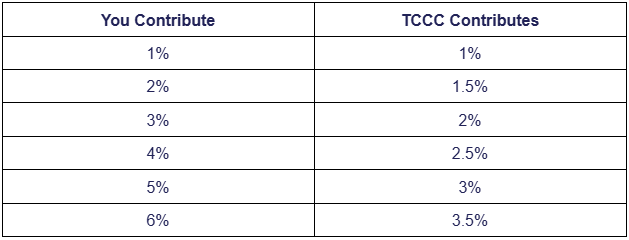

Understanding Your Coca-Cola 401k Match

TCCC matches 100% of your contributions up to 1% of your salary. After that, their match is a smaller percentage dependent on your total contribution.

Let’s take a look at this chart to understand how it works:

Ideally, you can contribute up to the maximum company match to take advantage of the funds your employer is willing to contribute to your retirement. If you skip this, you’re leaving money on the table. This can be a problem because, when it comes to saving for retirement, every little bit you’re able to put away counts!

What Can You Contribute?

Although TCCC doesn’t have any company-imposed contribution limits, the federal government limits how much you can contribute to your 401k each year. In 2025, the contribution limit is $23,500 per year if you’re under age 50. If you’re over age 50, you get to contribute an extra $7,500 annually as a “catch-up” contribution as you get closer to retirement. The employer match doesn’t count toward this limit – so it’s truly an “extra” contribution to your retirement savings.

Coca-Cola 401k Terms of Withdrawal

Withdrawals from your Coca-Cola Company 401k are subject to IRS rules. In most cases, you must be at least 59½ years old to take money out without facing extra charges. Taking funds out before then usually triggers a 10% early withdrawal fee on top of the income taxes you already owe.

Once you reach age 73, Required Minimum Distributions (RMDs) must start. You also may have access to 401k loans or hardship withdrawals under certain conditions, but these options can impact long-term growth, so it’s wise to plan carefully before using them.

Coca-Cola 401k Plan FAQs

1. Can I change my contributions after I enroll?

Yes, once you’re enrolled in the Coca-Cola Company 401k, you’re not locked into your initial choices. You’re free to adjust your contribution rate whenever you’d like to increase or decrease how much you’re putting away from each paycheck. This can be especially helpful as your income, budget, or retirement timeline shifts. You can also reallocate your investments based on your risk tolerance or market outlook by logging into the plan administrator’s portal.

2. Is the company match vested right away?

No, Coca-Cola’s employer contributions are subject to a vesting schedule. While your own contributions are always 100% yours from day one, the company match becomes yours over time. Typically, you become fully vested in Coca-Cola’s contributions after three years of service.

That means if you leave before reaching the vesting milestone, you may forfeit a portion of the match. If you plan to switch jobs or retire early, it’s a good idea to review your current vesting status through your 401k dashboard or plan documents to understand what you’re entitled to.

3. What happens if I leave the company?

If you leave Coca-Cola, your 401k doesn’t disappear—but what you do next can affect your long-term retirement strategy. You have several options: you can leave your funds in the Coca-Cola plan if your balance meets the minimum requirement, roll it over into a new employer’s 401k plan, or transfer it to a personal IRA.

Transferring your account to an IRA can give you broader investment choices and help simplify your retirement savings if you’ve switched jobs over the years. That said,to steer clear of taxes or penalties, it’s important to complete the rollover directly between accounts.

4. Can I contribute to both the 401k and an IRA?

Yes, contributing to both a 401k and an IRA is allowed and can be a smart way to increase your retirement savings. However, the ability to deduct traditional IRA contributions depends on your income level and whether you or your spouse participate in a workplace retirement plan like Coca-Cola’s 401k.

If your earnings are above certain limits, the deduction might be reduced or not allowed at all. Roth IRAs have their own income limits as well, so it’s wise to review current IRS guidelines or consult a financial professional to determine what combination of accounts is most beneficial for you.

5. Does the Coca-Cola 401k offer Roth contributions?

Yes, Coca-Cola’s 401k plan typically allows you to make Roth contributions in addition to traditional pre-tax ones. With a Roth 401k, you contribute money that’s already been taxed, so there’s no upfront deduction. The upside is that if you follow IRS guidelines, you can take out both your contributions and any growth completely tax-free in retirement.

This option can especially appeal to younger employees who expect their income and tax rates to rise over time or those who want to hedge against future tax increases. You also have the option to divide your contributions between Roth and traditional accounts, which can help balance your tax burden when it’s time to withdraw in retirement.

Maximizing Your Coca-Cola Company 401k With Expert Guidance

The Coca-Cola Company 401k offers a solid foundation for your retirement savings, especially when you understand how to make the most of its features. From maximizing your match to making strategic investment choices, the right approach can help you turn your 401k into a pillar of your retirement plan.

At Wealthcare for Women, I help Coca-Cola employees maximize their company benefits by creating personalized financial plans that integrate their 401k options, stock compensation, and long-term retirement goals. Whether you’re just starting out or approaching retirement, my goal is to help you make confident, well-informed choices about your financial path ahead.

Ready to make the most of your Coca-Cola Company 401k? Schedule a complimentary consultation with me today!